Turnkey Casino Solution: Full Operator Guide

Starting an online casino in 2026 doesn’t mean building everything from scratch. Turnkey casino solutions have transformed the iGaming industry, allowing entrepreneurs and established operators to launch fully functional platforms in weeks rather than years.

But here’s the reality, not all turnkey solutions are created equal. Some promise the world and deliver half-ba ked platforms. Others charge premium prices for outdated technology. The difference between choosing the right solution and the wrong one can mean the difference between a thriving operation and a costly failure.

In this comprehensive guide, we’ll walk you through everything you need to know about turnkey casino solutions—from understanding what they actually include to calculating real costs and avoiding common pitfalls that trap first-time operators.

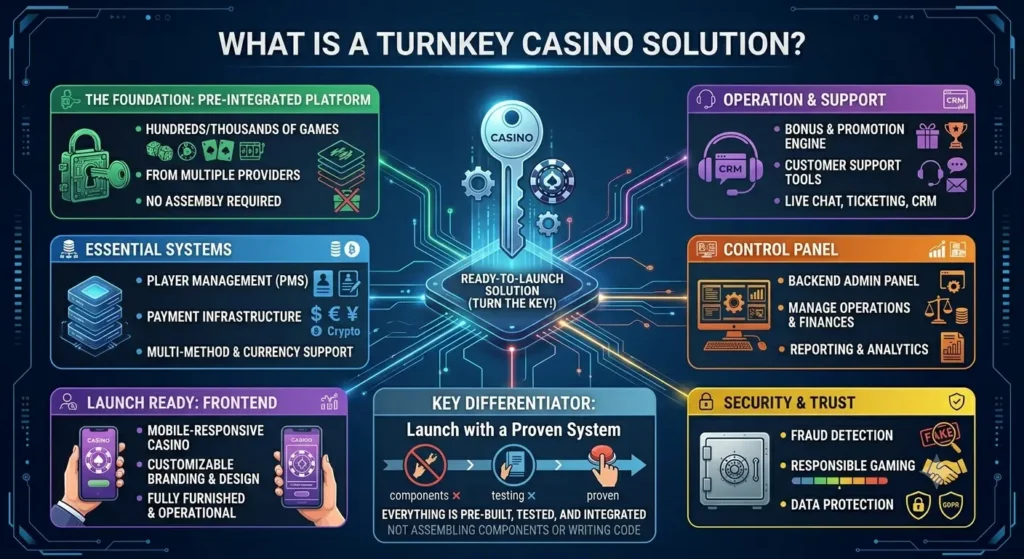

What Is a Turnkey Casino Solution?

A turnkey casino solution is a complete, ready-to-launch online casino platform that includes everything you need to start operating immediately. Think of it as buying a fully furnished, operational restaurant instead of building one from the ground up.

The term “turnkey” comes from the idea that you simply “turn the key” and start operating. In practice, it means you receive:

- Pre-integrated gaming platform with hundreds or thousands of games from multiple providers

- Payment processing infrastructure supporting various methods and currencies

- Player management system for registration, verification, and account handling

- Bonus and promotion engine to create and manage marketing campaigns

- Customer support tools including live chat, ticketing systems, and CRM

- Security features like fraud detection, responsible gaming controls, and data protection

- Backend administration panel for managing operations, finances, and reporting

- Mobile-responsive frontend with customizable branding and design

Key differentiator? Everything is pre-built, tested, and integrated. You’re not assembling components from different vendors or writing code—you’re launching with a proven system.

Turnkey vs. White Label vs. Custom Development

Before diving deeper, let’s clarify how turnkey solutions compare to other approaches:

| Approach | Initial Market Cost | Customization | Control Level | Best For |

| Turnkey Solution | $30,000-$150,000 | Moderate (branding, themes, game selection) | Medium | First-time operators, rapid market entry |

| White Label | $15,000-$80,000 + revenue share | Limited (surface-level branding) | Low | Low-budget startups, testing markets |

| Custom Development | $500,000-$5,000,000+ | Complete | Full | Established operators, unique requirements |

Turnkey solutions offer the sweet spot for most operators. You get more control and customization than white label, without the astronomical costs and lengthy timelines of custom development.

White label platforms are cheaper upfront but typically require ongoing revenue sharing (15-30% of gross gaming revenue), which can become extremely costly as you scale. You’re also limited in how you can differentiate your brand.

Custom development gives you complete control but requires significant capital, technical expertise, and patience. Unless you’re targeting a unique niche or have substantial backing, it’s often overkill for entering the market.

Core Components of a Professional Turnkey Casino Platform

Furthermore, a quality turnkey solution isn’t just about games and payments. Let’s break down the essential components:

1. Game Integration and Management

The heart of any casino is its game library. Professional turnkey platforms include:

- Multi-provider integration: Access to 50+ game providers (NetEnt, Pragmatic Play, Evolution Gaming, etc.)

- Game aggregation platform: Unified API managing all providers through one integration

- 10,000+ games: Slots, table games, live dealer, sports betting, virtual sports

- Automatic updates: New games added automatically as providers release them

- Game management tools: Categorization, featured games, jackpot tracking

What to watch for: Some providers offer “integrated” games that are actually just iframes with limited control. Look for true API integration with full reporting and player tracking.

2. Payment Gateway Infrastructure

Money movement is critical. Expect these capabilities:

- 50-100+ payment methods: Credit/debit cards, e-wallets, crypto, bank transfers, local methods

- Multi-currency support: 20-50 currencies with automatic conversion

- Instant deposits: Real-time processing for most payment methods

- Flexible withdrawal processing: Automatic, manual, or hybrid approval workflows

- Anti-fraud measures: Velocity checks, duplicate detection, risk scoring

- KYC/AML integration: Document verification, screening against sanctions lists

Reality check: Payment processing is often where hidden costs lurk. Transaction fees (3-8% for cards, lower for alternative methods) aren’t included in platform fees.

3. Player Management System (PMS)

Your PMS handles the entire player lifecycle:

- Registration and onboarding: Customizable signup forms, email verification

- Identity verification: Document upload, facial recognition, automated checks

- Account management: Balance tracking, transaction history, limits setting

- Segmentation tools: Group players by activity, value, location, behavior

- Communication engine: Email, SMS, push notifications with automation

- Responsible gaming controls: Deposit limits, time-outs, self-exclusion

4. Bonus and Campaign Engine

Marketing tools integrated into your platform:

- Welcome bonuses: First deposit matches, free spins packages

- Ongoing promotions: Reload bonuses, cashback, tournaments

- VIP programs: Tiered systems with point accumulation

- Gamification: Achievements, missions, leaderboards

- Personalization: Targeted offers based on player behavior

- Budget controls: Cap exposure, track marketing spend ROI

5. Back Office and Reporting

Command center for your operation:

- Real-time dashboard: Key metrics at a glance (GGR, NGR, active players, deposits)

- Financial reports: Detailed P&L, player balances, liability tracking

- Player analytics: Behavior patterns, LTV calculations, churn prediction

- Compliance reporting: Suspicious activity reports, responsible gaming metrics

- Audit trails: Complete transaction logs for regulatory requirements

- Multi-user access: Role-based permissions for team members

6. Security and Compliance Features

Non-negotiable elements for licensed operation:

- SSL/TLS encryption: 256-bit encryption for data transmission

- Secure storage: Encrypted databases, secure file storage

- Session management: Automatic timeouts, IP tracking, device fingerprinting

- RNG certification: Certified random number generators for fair play

- Regulatory compliance tools: Jurisdiction-specific features (UK, Malta, Curacao)

- Data protection: GDPR compliance, data retention policies, right-to-erasure tools

The Real Cost of Turnkey Casino Solutions

Let’s talk numbers. Marketing materials often show attractive monthly fees, but the total cost of ownership is more complex.

Upfront Costs

| Cost Category | Market Range | Notes |

| Platform Setup Fee | $20,000-$100,000 | One-time integration, configuration, branding |

| License Application | $10,000-$50,000 | Varies by jurisdiction (Curacao cheaper, Malta/UK expensive) |

| Initial Game Provider Deposits | $10,000-$50,000 | Security deposits required by most providers |

| Legal and Consulting | $5,000-$25,000 | Company formation, compliance advice |

| Marketing Launch Budget | $50,000-$200,000 | First 3-6 months of acquisition |

| Working Capital | $100,000-$500,000 | Cover player balances, operational costs |

Realistic total to launch: $195,000-$925,000

Monthly Market Operating Costs

| Expense | Monthly Range | Annual Range |

| Platform License Fee | $5,000-$25,000 | $60,000-$300,000 |

| Game Provider Fees | Revenue share: 10-15% of GGR | Variable |

| Payment Processing | 3-8% of transaction volume | Variable |

| Hosting and Infrastructure | $2,000-$10,000 | $24,000-$120,000 |

| Support and Maintenance | $3,000-$15,000 | $36,000-$180,000 |

| License Renewal | $1,000-$4,000 | $12,000-$48,000 |

| Staff (minimum team) | $15,000-$40,000 | $180,000-$480,000 |

| Marketing | $20,000-$100,000+ | $240,000-$1,200,000+ |

Important: Some providers charge flat monthly fees, others take revenue share (5-15% of GGR), and many use hybrid models. Calculate which works better based on your projected volumes.

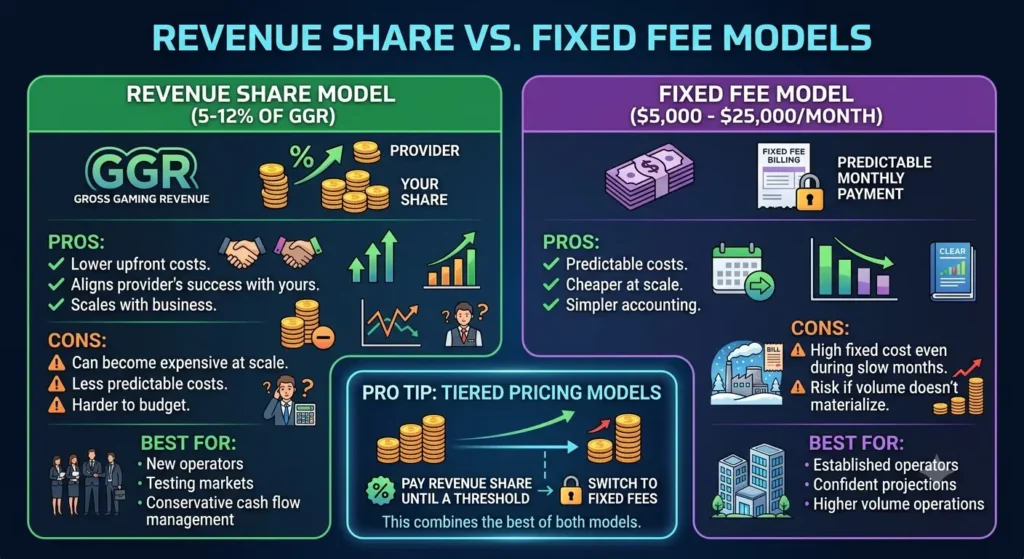

Revenue Share vs. Fixed Fee Models

Revenue Share Model (5-12% of GGR):

- Pros: Lower upfront costs, aligns provider’s success with yours, scales with business

- Cons: Can become expensive at scale, less predictable costs, harder to budget

- Best for: New operators, testing markets, conservative cash flow management

Fixed Fee Model ($5,000-$25,000/month):

- Pros: Predictable costs, cheaper at scale, simpler accounting

- Cons: High fixed cost even during slow months, risk if volume doesn’t materialize

- Best for: Established operators, confident projections, higher volume operations

Pro tip: Some providers offer tiered pricing where you pay revenue share until a certain threshold, then switch to fixed fees. This combines the best of both models.

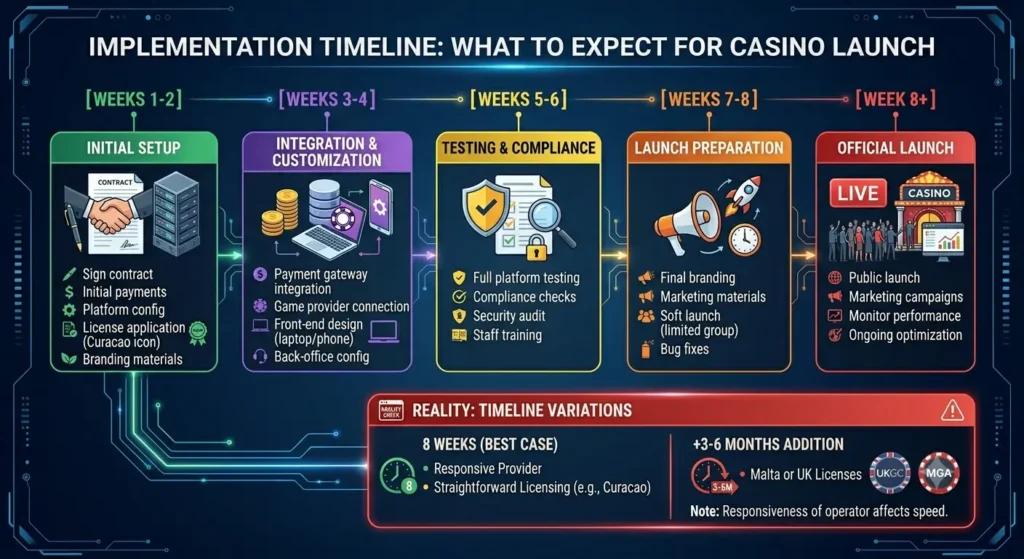

Implementation Timeline: What to Expect

Understanding the realistic timeline helps you plan launch dates and coordinate marketing:

Weeks 1-2: Initial Setup

- Sign contract and make initial payments

- Platform configuration begins

- Choose jurisdiction and start license application

- Provide branding materials (logo, colors, copy)

Weeks 3-4: Integration and Customization

- Payment gateways integrated and tested

- Game providers connected (typically 20-50 initially)

- Front-end customization (website design, user flows)

- Back-office configuration for your team

Weeks 5-6: Testing and Compliance

- Full platform testing (functionality, payments, games)

- Compliance checks and responsible gaming features

- Security audit and penetration testing

- Staff training on back-office systems

Weeks 7-8: Launch Preparation

- Final branding adjustments

- Marketing materials prepared

- Soft launch with limited audience

- Bug fixes and optimization

Week 8+: Official Launch

- Public launch with marketing campaigns

- Monitor performance and player feedback

- Ongoing optimization and game additions

Reality: 8 weeks is the best-case scenario with a responsive provider and straightforward licensing (Curacao). Malta or UK licenses can add 3-6 months to the timeline.

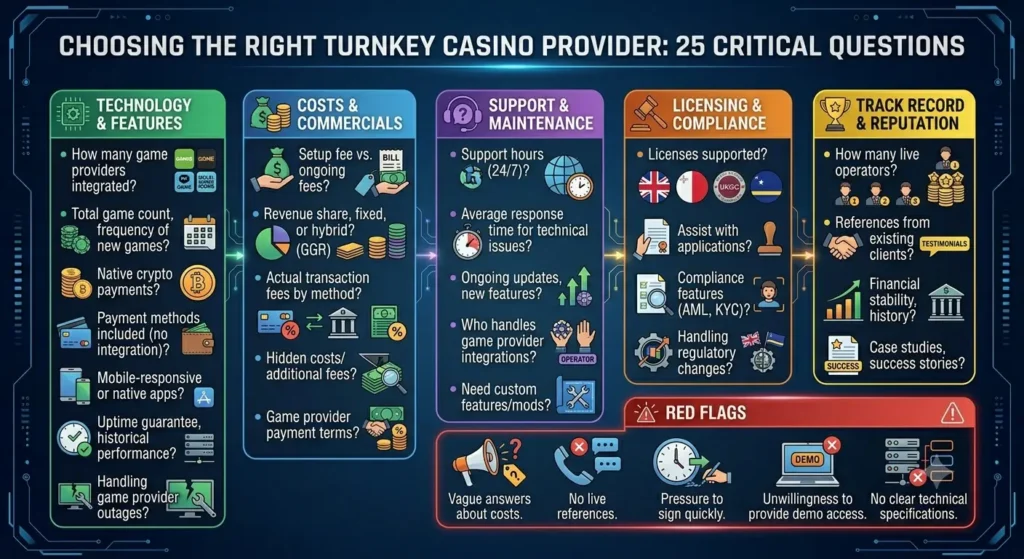

Choosing the Right Turnkey Casino Provider

Not sure which provider to trust? Ask these questions before signing:

Technology and Features

- How many game providers are integrated, and which specific ones?

- What’s the total game count, and how often are new games added?

- Does the platform support crypto payments natively?

- What payment methods are included without additional integration?

- Is the platform mobile-responsive or do you provide native apps?

- What’s your platform uptime guarantee and historical performance?

- How do you handle game provider outages or technical issues?

Costs and Commercials

- What’s included in the setup fee vs. ongoing fees?

- Do you charge revenue share, fixed fees, or hybrid?

- What are the actual transaction fees for different payment methods?

- Are there any hidden costs or additional fees I should know about?

- What payment terms do game providers require (deposits, revenue share)?

Support and Maintenance

- What support hours do you offer (24/7, business hours, timezone)?

- What’s your average response time for technical issues?

- Do you provide ongoing updates and new features?

- Who handles game provider integrations—your team or mine?

- What happens if I need custom features or modifications?

Licensing and Compliance

- Which licenses does your platform support?

- Do you assist with license applications?

- What compliance features are built-in (AML, KYC, responsible gaming)?

- How do you handle regulatory changes and updates?

Track Record and Reputation

- How many live operators are using your platform currently?

- Can you provide references from existing clients?

- What’s your company’s financial stability and history?

- Do you have any case studies or success stories to share?

Red flags: Vague answers about costs, no live references, pressure to sign quickly, unwillingness to provide demo access, no clear technical specifications.

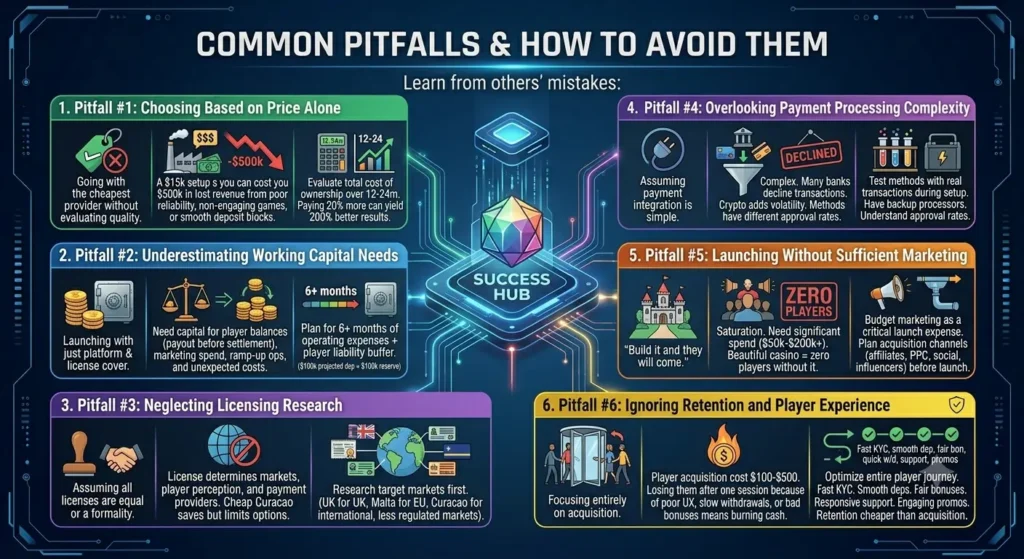

Common Pitfalls and How to Avoid Them

Learn from others’ mistakes:

Firstly, Pitfall #1: Choosing Based on Price Alone

The mistake: Going with the cheapest provider without evaluating quality.

Reality: A $15,000 setup saving you upfront can cost you $500,000 in lost revenue if the platform is unreliable, the games aren’t engaging, or players can’t deposit smoothly.

How to avoid: Evaluate the total cost of ownership over 12-24 months, including opportunity costs of poor performance. Sometimes paying 20% more for a superior platform yields 200% better results.

Secondly, Pitfall #2: Underestimating Working Capital Needs

The mistake: Launching with just enough money to cover platform and license.

Reality: You need capital to cover player balances (you pay out before game providers settle), marketing spend, operational costs during ramp-up, and unexpected expenses.

How to avoid: Plan for at least 6 months of operating expenses plus a buffer for player liability. If you’re projecting $100,000 in monthly player deposits, have at least that much in reserve.

Thirdly, Pitfall #3: Neglecting Licensing Research

The mistake: Assuming all licenses are equal or that licensing is just a formality.

Reality: Your license determines which markets you can legally operate in, how players perceive you, and which payment providers will work with you. A cheap Curacao license might save money but limit your options.

How to avoid: Research target markets first, then choose the appropriate license. UK license for UK players. Malta for European markets. Curacao for international but less regulated markets.

Fourth, Pitfall #4: Overlooking Payment Processing Complexity

The mistake: Assuming payment integration is simple and that advertised payment methods will all work smoothly.

Reality: Payment processing in iGaming is complex. Many banks decline gambling transactions. Different methods have different approval rates. Crypto adds volatility risk.

How to avoid: Test payment methods with real transactions during the setup phase. Have backup payment processors. Understand actual approval rates, not just technical integration.

Fifth, Pitfall #5: Launching Without Sufficient Marketing

The mistake: “Build it and they will come” mentality.

The reality: The iGaming market is saturated. Without significant marketing spend ($50,000-$200,000 for initial months), your beautifully designed casino will have zero players.

How to avoid: Budget marketing as a critical launch expense, not an afterthought. Plan your acquisition channels (affiliates, PPC, social media, influencers) before launch.

Sixth, Pitfall #6: Ignoring Retention and Player Experience

The mistake: Focusing entirely on acquisition without retention strategy.

The reality: Acquiring a player costs $100-$500. Losing them after one session because of poor UX, slow withdrawals, or bad bonuses means burning cash.

How to avoid: Optimize the entire player journey. Fast KYC. Smooth deposits. Fair bonuses. Quick withdrawals. Responsive support. Engaging promotions. Retention is cheaper than acquisition.

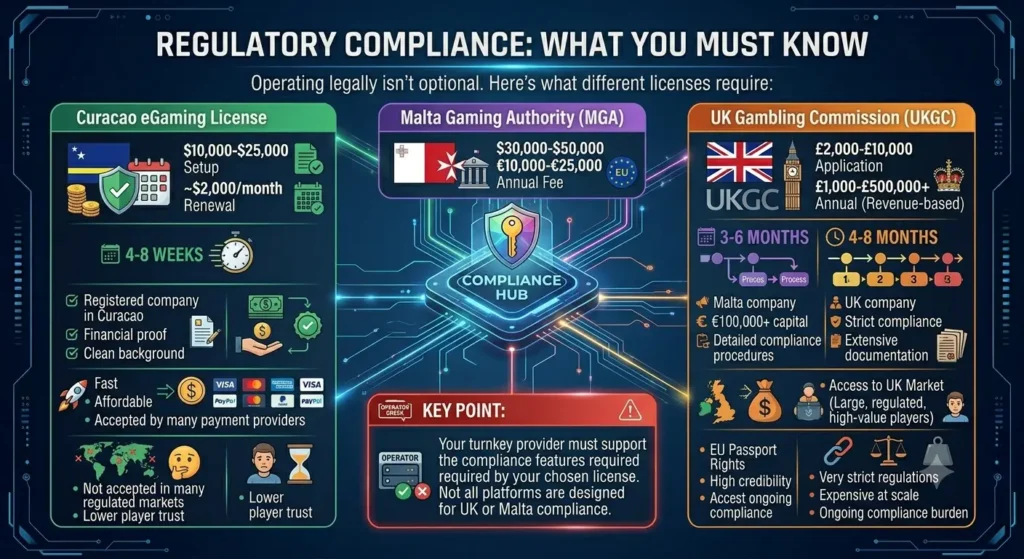

Regulatory Compliance: What You Must Know

Operating legally isn’t optional. Here’s what different licenses require:

Curacao eGaming License

- Cost: $10,000-$25,000 setup, ~$2,000/month renewal

- Timeline: 4-8 weeks

- Requirements: Registered company in Curacao, financial proof, clean background

- Advantages: Fast, affordable, accepted by many payment providers

- Limitations: Not accepted in many regulated markets, lower player trust

Malta Gaming Authority (MGA)

- Cost: $30,000-$50,000 setup, €10,000-€25,000 annual fee

- Timeline: 3-6 months

- Requirements: Malta company, €100,000+ capital, detailed compliance procedures

- Advantages: EU passport rights, high credibility, access to major markets

- Limitations: Expensive, lengthy process, strict ongoing compliance

UK Gambling Commission (UKGC)

- Cost: £2,000-£10,000 application, £1,000-£500,000+ annual (revenue-based)

- Timeline: 4-8 months

- Requirements: UK company, strict compliance, extensive documentation

- Advantages: Access to UK market (large, regulated, high-value players)

- Limitations: Very strict regulations, expensive at scale, ongoing compliance burden

Key point: Your turnkey provider must support the compliance features required by your chosen license. Not all platforms are designed for UK or Malta compliance.

Why Operators Choose Our Turnkey Solution

Moreover, at DSTGAMING, we’ve built our turnkey casino solution based on feedback from over 200 operators who’ve launched with us since 2018. Here’s what makes our platform different:

Battle-Tested Technology

Our platform powers casinos processing over $2 billion annually. It’s been stress-tested by peak traffic, proven in multiple jurisdictions, and refined through thousands of iterations based on real operator feedback.

Transparent Pricing, No Surprises

We believe in honest commercials. Our pricing is clear from day one: setup costs, monthly fees, revenue share percentages, and payment processing fees are all documented. No hidden charges six months after launch.

True Multi-Currency and Crypto Support

Native support for 45+ fiat currencies and 12 cryptocurrencies (Bitcoin, Ethereum, USDT, and more). Real-time conversion, automatic settlement, and regulatory-compliant crypto handling.

70+ Integrated Game Providers

Pre-integrated access to industry leaders: Evolution Gaming, Pragmatic Play, NetEnt, Playtech, Microgaming, and 65+ more. Over 12,000 games available from day one, with 50-100 new titles added monthly.

Launch in 4 – 6 Weeks

Our streamlined onboarding process gets you to market faster. We handle game provider negotiations, payment gateway integration, compliance setup, and platform configuration so you can focus on your business strategy.

Dedicated Success Team

You’re not just a client—you’re a partner. Each operator gets a dedicated account manager, 24/7 technical support, and access to our team of iGaming specialists who help you optimize and grow.

Ready to start your casino? Contact our team for a personalized demo and see how DSTGAMING can power your success.

Turnkey Casino Success Stories

Case Study 1:

Challenge: First-time operator wanted to launch a crypto-focused casino targeting European and Asian markets within 3 months.

Solution: DSTGAMING platform with enhanced crypto payment integration, 50+ providers, Malta license application support.

Results:

- Launched in 9 weeks (including 1-week delay for additional customization)

- $1.2M in deposits first month

- 4,200 registered players in 90 days

- 42% player retention rate (industry average: 25-30%)

Key factor: Strong crypto payment integration and rapid game provider onboarding helped them enter the market before competitors.

Advanced Features to Look For

As you evaluate providers, consider these advanced capabilities that separate basic platforms from enterprise-grade solutions:

Player Intelligence and Analytics

- Behavioral tracking: Monitor player patterns, identify at-risk gambling behavior

- LTV prediction: AI-powered lifetime value forecasting for better marketing ROI

- Churn prevention: Automated triggers to engage players showing drop-off signals

- Segment automation: Dynamic player grouping based on real-time behavior

Marketing Automation

- Journey mapping: Automated email/SMS flows based on player actions

- A/B testing: Built-in split testing for bonuses, landing pages, messaging

- Personalized offers: AI-generated promotions based on individual preferences

- Attribution tracking: Know exactly which channels drive your best players

Multi-Brand Management

- Single platform, multiple brands: Run several casino brands from one backend

- Shared player pools: Cross-brand promotions and unified player management

- Brand-specific configurations: Different games, bonuses, designs per brand

- Consolidated reporting: See performance across all brands in one dashboard

White Label Network Benefits

- Shared liquidity: Combine player pools for larger jackpots and tournaments

- Group marketing: Benefit from network-level marketing initiatives

- Provider negotiations: Better rates through collective bargaining

- Shared infrastructure costs: Economy of scale on technology investments

Next Steps: Your Path to Launch

Ready to move forward? Here’s your action plan:

Month 1: Research and Planning

- Define your target market and player demographics

- Research licensing requirements for target jurisdictions

- Create financial projections (realistic ones)

- Evaluate 3-5 turnkey providers using our 25 questions

- Assemble your core team (marketing, operations, customer support)

Month 2: Provider Selection and Legal Setup

- Request demos from shortlisted providers

- Negotiate commercials and review contracts thoroughly

- Engage legal counsel specializing in iGaming

- Begin company formation in chosen jurisdiction

- Start license application process

Month 3: Platform Setup and Integration

- Sign provider agreement and make initial payments

- Provide branding materials and design preferences

- Configure game selection and payment methods

- Set up back-office user accounts and permissions

- Begin staff training on platform

Month 4: Testing and Marketing Preparation

- Comprehensive platform testing (functionality, payments, games)

- Security audit and compliance check

- Finalize marketing strategy and materials

- Set up affiliate program and partnerships

- Prepare customer support workflows and scripts

Month 5: Soft Launch and Optimization

- Limited launch to test real-money operations

- Monitor technical performance and player feedback

- Optimize payment flows and KYC processes

- Final adjustments based on early data

- Prepare for full-scale marketing campaigns

Month 6: Official Launch

- Public launch with marketing blitz

- Monitor KPIs closely (registration rate, FTD conversion, retention)

- Engage with early players for feedback

- Adjust bonuses and promotions based on performance

- Scale marketing based on initial results

The realistic timeline is 6-12 weeks from signing the contract to going live, depending on licensing jurisdiction. Curacao licenses can be obtained in 4-6 weeks, allowing for faster launches. Malta or UK licenses extend the timeline to 3-6 months due to more rigorous application processes.

You should have at least $200,000-$300,000 in total capital. This includes platform setup ($30,000-$60,000), licensing ($10,000-$50,000), initial game provider deposits ($20,000-$40,000), and working capital ($100,000-$150,000) for the first 3-6 months of operations.

Yes. Most turnkey providers allow you to start with 20-30 game providers (still thousands of games) and add more as you grow. This reduces initial costs and complexity while giving you time to understand which games perform best with your players.

No extensive technical knowledge is required. The platform handles all technical aspects. You need business acumen, understanding of iGaming operations, marketing skills, and customer service capabilities. Most providers offer training and ongoing support for the technical side.

Managed services: Provider handles day-to-day operations (customer support, payment processing, fraud management) in exchange for higher revenue share (20-40% of GGR). Lower stress, but less control and higher long-term costs.

Self-operated: You run all operations using the platform. Lower revenue share (5-15%), more control, but requires hiring a team and managing operations yourself.

Choose revenue share if: You’re risk-averse, have limited upfront capital, are testing a market, or project modest initial volumes (under $500,000 monthly deposits).

Choose a fixed fee if: You project high volumes (over $1,000,000 monthly deposits), want predictable costs, have strong capital backing, or plan to scale aggressively.

Technically yes, but it’s extremely complex and costly. Migrating player databases, re-integrating payment methods, transferring game histories, and maintaining player balances makes switching very difficult. Choose carefully from the start—treat it like a 3-5 year commitment.

This occasionally happens due to licensing changes or provider decisions. Quality turnkey platforms have contracts with 50+ providers specifically to mitigate this risk. If one provider leaves, you still have thousands of games from others. The platform provider typically handles the technical removal and player notifications.

Modern turnkey platforms include built-in responsible gaming tools: deposit limits (daily/weekly/monthly), time-based limits, self-exclusion options, reality checks, and cool-off periods. These are typically required by licenses and can be configured based on jurisdiction requirements.

This varies widely. Some providers offer only the platform. Others provide affiliate network access, marketing materials, SEO support, and even managed marketing services. DSTGAMING offers affiliate network integration, marketing material templates, and strategic guidance as part of our standard package.

Yes. A quality turnkey platform supports multi-jurisdiction operations through geo-targeting, multiple currencies, localized content, and jurisdiction-specific compliance features. However, you may need multiple licenses depending on which regulated markets you target.

Game providers typically charge 10-15% of GGR from their games. This is in addition to your platform fee. So if your platform charges 8% revenue share and game providers charge 12%, your total cost is ~20% of GGR. Fixed fee models eliminate this stacking.

Is a Turnkey Casino Solution Right for You?

After exploring the landscape of turnkey casino solutions, here’s the bottom line:

Turnkey is ideal if you:

- Want to launch quickly (within 1 – 2 months)

- Have $200,000-$500,000 in capital

- Prefer proven technology over custom development

- Need a complete solution without assembling multiple vendors

- Want to focus on marketing and operations rather than technical development

Consider alternatives if you:

- Have very unique requirements that require extensive customization

- Already have established technical infrastructure

- Are targeting only niche markets with specific needs

- Have budget constraints below $150,000 total

iGaming industry is competitive and fast-moving. Turnkey solutions exist because they work—they allow you to launch faster, reduce technical risk, and focus on what really matters: acquiring and retaining players.

The key to success isn’t just choosinug any trnkey provider. It’s choosing the right provider for your specific market, budget, and ambitions. Do your research, ask tough questions, verify claims with existing clients, and don’t rush the decision.

Furthermore, at DSTGAMING, we’ve helped hundreds of operators launch successful casinos across multiple jurisdictions and markets. Whether you’re a first-time operator or an experienced business expanding online, our turnkey solution provides the technology foundation for long-term success.

Ready to explore your options? Schedule a personalized consultation with our team. We’ll review your business plan, discuss your target market, and show you exactly how our platform can support your vision.

About DSTGAMING: We’ve been providing enterprise-grade iGaming solutions since 2018, powering over 200 successful online casinos across 45 countries. Our turnkey platform combines cutting-edge technology with operational expertise to help operators launch faster, operate smoother, and grow bigger.

Contact: Request a demo | Get pricing | Talk to an expert